Lowe’s reported fourth quarter and full-year fiscal 2025 results for the period ending January 30, 2026, posting positive comparable sales in Q4 and outlining a full-year 2026 outlook that signals confidence despite continued uncertainty in the home improvement market.

Inside the Results

Q4 fiscal 2025 highlights

- Total sales: $20.6B vs. $18.6B last year

- Comparable sales: up 1.3%

- Net earnings: $1.0B

- Diluted EPS: $1.78 vs. $1.99 last year

- Adjusted diluted EPS: $1.98, up 2.6% year over year (excludes $149M pretax acquisition-related expenses)

- Comp transactions: down 2.3%

- Comp average ticket: up 3.6% to $107.28

- Online sales growth: up 10.5%

- Margin snapshot: gross margin 32.5% (down 40 bps) and operating margin 8.3% (down 157 bps); adjusted operating margin was 9.0% (down 41 bps).

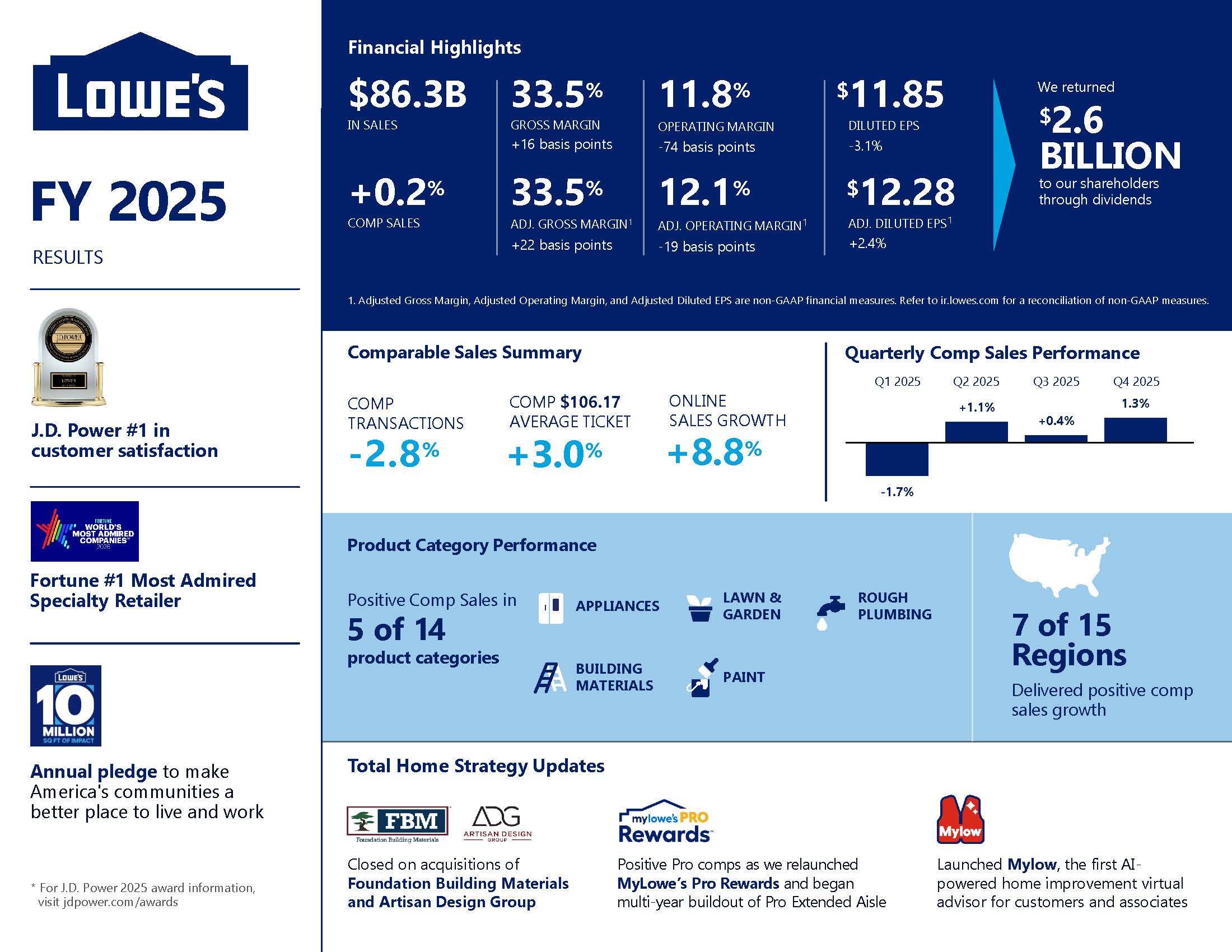

Full-year fiscal 2025 highlights

- Total sales: $86.3B

- Comparable sales: up 0.2%

- Diluted EPS: $11.85, down 3.1%

- Adjusted diluted EPS: $12.28, up 2.4%

- Returned to shareholders via dividends: $2.6B for the year

What Drove the Quarter

Lowe’s positioned the quarter as evidence that its Total Home strategy is resonating with both Pro and DIY shoppers, supported by strong holiday performance and continued growth in Pro, online and home services.

A few additional callouts from the Q4 results:

- Positive comp sales in 12 of 15 regions

- Positive comp sales in 9 of 14 product categories

- A “record-setting” Black Friday and Cyber Monday weekend supported by the Lowe’s Creator Network

- Completed pet and workwear rollout to 1,000 stores

- Awarded $125M in discretionary bonuses to frontline associates

Outlook and Implications for Suppliers and Brands

Lowe’s introduced full-year fiscal 2026 guidance that reflects ongoing uncertainty in the market while still projecting meaningful growth off the fiscal 2025 base.

Full-year 2026 outlook highlights

- Total sales: $92.0B to $94.0B

- Comparable sales: flat to up 2%

- Operating margin: 11.2% to 11.4%

- Adjusted operating margin: 11.6% to 11.8%

- Diluted EPS: $11.75 to $12.25

- Adjusted diluted EPS: $12.25 to $12.75

- Capex: approximately $2.5B

For home improvement brands and suppliers, the takeaway is that Lowe’s is leaning into growth levers that reward strong execution:

- Pro is a clear engine, so build Pro-ready stories: Lowe’s cited continued Pro growth as a driver of Q4 comp sales. Suppliers should align assortments, value props and education to Pro needs like durability, jobsite efficiency and reliable replenishment.

- Online demand is up, so the digital shelf is not optional: With online sales growth up 10.5% in Q4, findability and clarity matter. Tight PDP content, strong imagery and project-based guidance can convert mission shoppers faster.

- Traffic pressure means basket-building matters more: Transactions were down while ticket was up. Help shoppers complete the job by making companion items obvious, easy to shop and easy to understand.

Porchlight’s Perspective

At Porchlight, we read Lowe’s results as a sign that shoppers are still selective, but brands can grow by leaning into Pro demand, tightening digital shelf execution, and merchandising around clear project solutions that lift ticket and conversion.

Additional Resources

Lowe’s Q4 2025 Earnings Report and FY 2025 Results